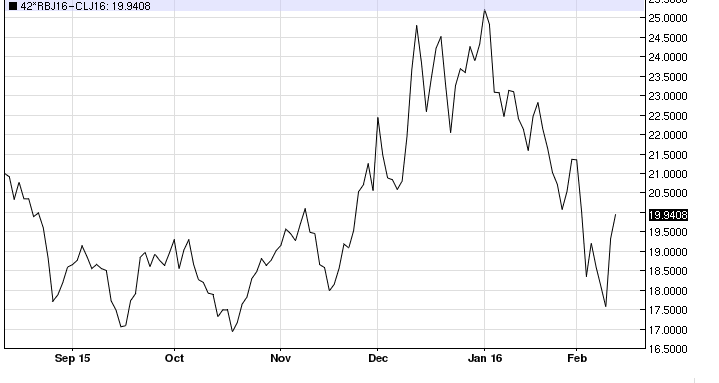

The EIA reported this week that gasoline stocks had assaulted another record high at 255.7 million barrels. Gasoline inventories have built by almost 35 million barrels over the past five weeks thanks to refiners running their plants in a max gasoline mode in order to capture a healthy gasoline margin. Mid-continent plants ran at an astounding 97 percent capacity in January and as a result lifted supply in Pad 2 by 11 million barrels to a bloated 61 million barrels or 8 million over last year. The surplus of gasoline and in particular winter grade led to Chicago and Group 3 cash markets trading as low as 30 to 40 cents under he NYMEX nearby gasoline market. In other words mid con wholesale gasoline prices were close in the 60 cent per gallon range. Gasoline cracks in the mid continent fell to under a dollar per gallon versus West Texas Intermediate. In the face of weakening margins a few refiners have announced economic run cuts ,while others are rumored to be on the verge (you first!). In any event the talk of run cuts coupled with the real prospect of turnarounds helped to rally the April gasoline by over 2 dollars per gallon over the past two sessions.(Chart below)

While we would not be at all surprised to see the April gasoline crack rally to the 21.50 to 23.00 area,we do think it will be difficult to sustain much above those levels. Inventories have much too far to draw down to reach normal end February levels (232 million) or end March levels (224 million barrels). We see this rally as corrective for now, a true recovery is going to take some time.

Leave a Reply