Here is the EIA’s “Today in Energy“:

“As crude oil production in the Permian Basin of western Texas and eastern New Mexico has increased, pipeline infrastructure has also increased to deliver this crude oil to demand centers on the U.S. Gulf Coast.

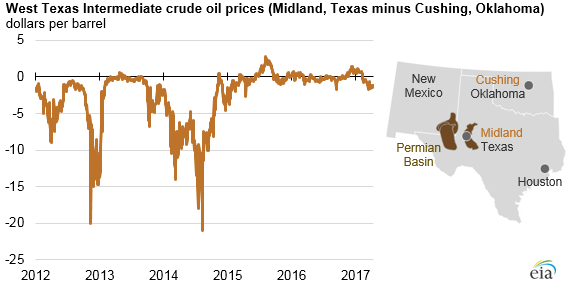

One indicator of a potential shortfall in available takeaway capacity in the Permian is a negative spread between the price of West Texas Intermediate (WTI) crude oil at Midland, Texas, and the price of WTI at Cushing, Oklahoma.

Going forward, the Midland versus Cushing discount, which recently widened to more than $1 per barrel (b), is unlikely to be either as large or as persistent as it was following the rapid increase in Permian production from 2010 to 2014. At points in both late 2012 and mid-2014, WTI-Midland was priced at least $15/b lower than WTI-Cushing. Pipeline capacity expansions and other market changes are now underway to deliver more Permian crude oil to demand centers.”

Here is the Midland/Cushing price spread:

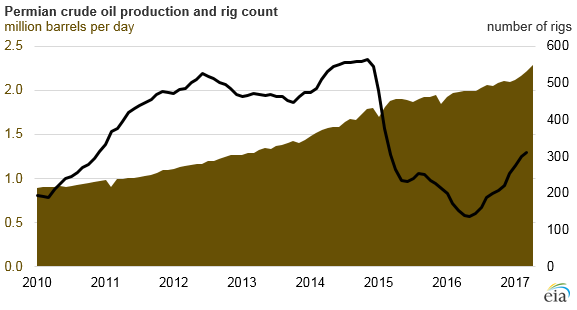

“With the rise in oil prices from their low point in early 2016, EIA’s April Short-Term Energy Outlook (STEO) expects crude oil production growth in the Permian to accelerate. EIA’s April Drilling Productivity Report (DPR) indicates a total of 310 oil-directed rigs active in the Permian, 158 more than at the same time last year. The DPR also estimates crude oil production in the Permian at 2.3 million b/d as of April 2017, or almost 300,000 b/d higher than the same month in 2016.”

Leave a Reply