The EIA’s Short Term Energy Outlook, here, was released today… Here are some interesting words and charts:

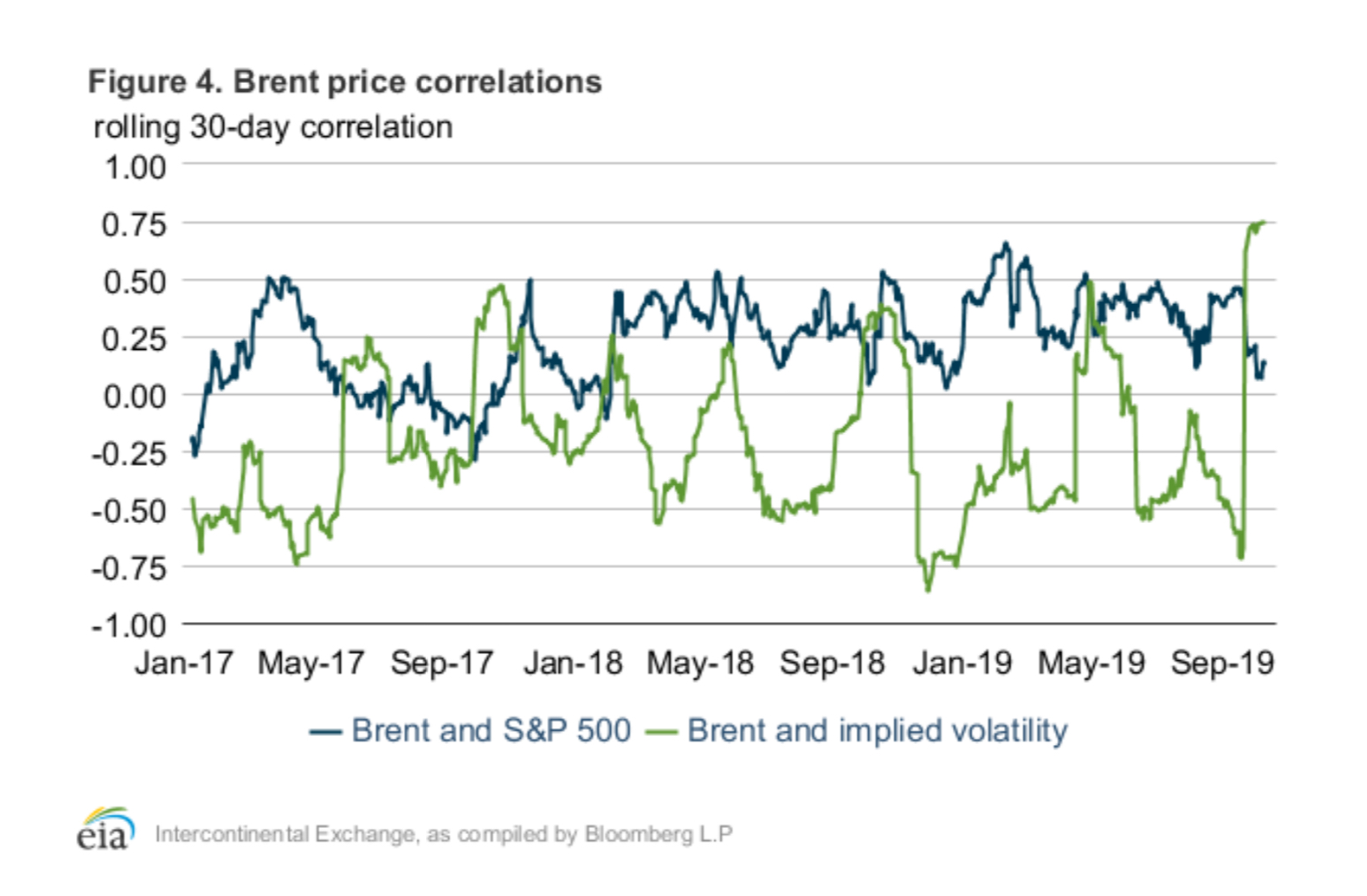

”Increases in both crude oil prices and implied volatility are typical during supply disruptions. Most of the time, crude oil prices and implied volatility exhibit little or slightly negative correlation. During a crude oil supply disruption, however, market participants must seek alternative sources of supply amid an environment of uncertain price direction and supply availability, contributing to increases in prices and volatility. The rolling 30-day correlation between Brent prices and implied volatility increased to more than 0.7 in the days following the attack on Saudi oil infrastructure, a strong degree of positive correlation witnessed during other periods of crude oil supply disruptions during the past two years (Figure 4). In contrast, the correlation between Brent prices and the S&P 500—which had exhibited moderately high positive correlation since early 2018—declined to almost zero correlation by the first week of October. These two assets tend to exhibit positive correlation when demand-side factors, such as global economic growth, are contributing to crude oil price formation. Now that Saudi Araba’s crude oil production has returned to pre-attack levels, information concerning global economic growth could reemerge as the main contributor to crude oil price formation.”

Leave a Reply