The always excellent RBN Energy covers recent developments in LNG, here…

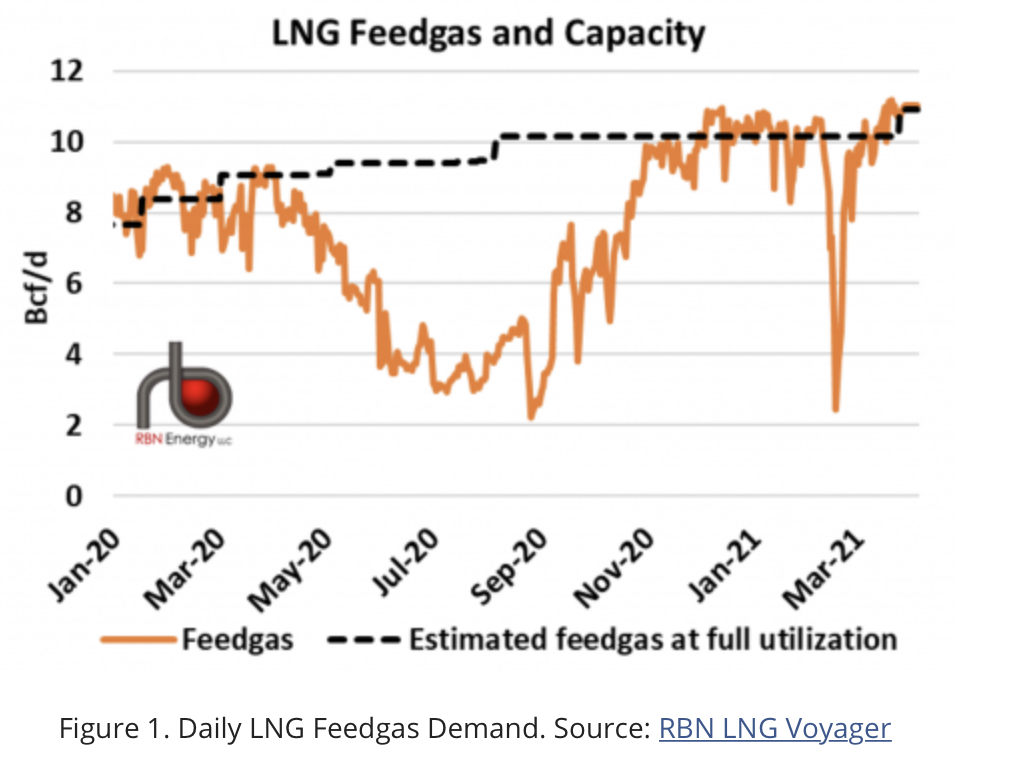

”As we discussed recently in Wild Thing, feedgas demand and U.S. LNG production over the past year faced unprecedented volatility, first because of economically driven cargo cancellations due to COVID-19 and the subsequent crash in prices globally (see Break It to Me Gently, Undone and LNG Interruption for more). Then, later last year, just as global demand and prices were rising again, a record-setting hurricane season wreaked havoc on the operations of Gulf Coast LNG terminals, particularly in Louisiana, hampering exports (see You Spin Me Round). Feedgas consumption recovered by winter, but the Gulf Coast terminals continued to see intermittent disruptions, even as global prices and demand remained strong. Earlier this year, we saw a slowdown in exports, albeit relatively modest, stemming from constraints on passage through the Panama Canal, which in turn led to voyage delays and a vessel shortage. Then came Winter Storm Uri, which created a severe gas shortage in Texas and curtailed production as export facilities sent gas back into the market to help meet domestic demand (see Feed Me). That was followed by a period of foggy conditions along the Gulf Coast that intermittently interrupted marine traffic. However, as the weather turned warmer, most facilities returned to full operating capacity and feedgas demand rebounded. Feedgas consumption averaged about 10.9 Bcf/d in the second half of March (orange line in Figure 1) after peaking above 11 Bcf/d on multiple days and breaking the single-day record three times as Corpus Christi Train 3 reached the final days of its commissioning and entered service on March 26. In the first few days of April, feedgas volumes have continued to top 11 Bcf/d.”

Leave a Reply