Here are some highlights from the EIA’s monthly Short Term Energy Outlook…

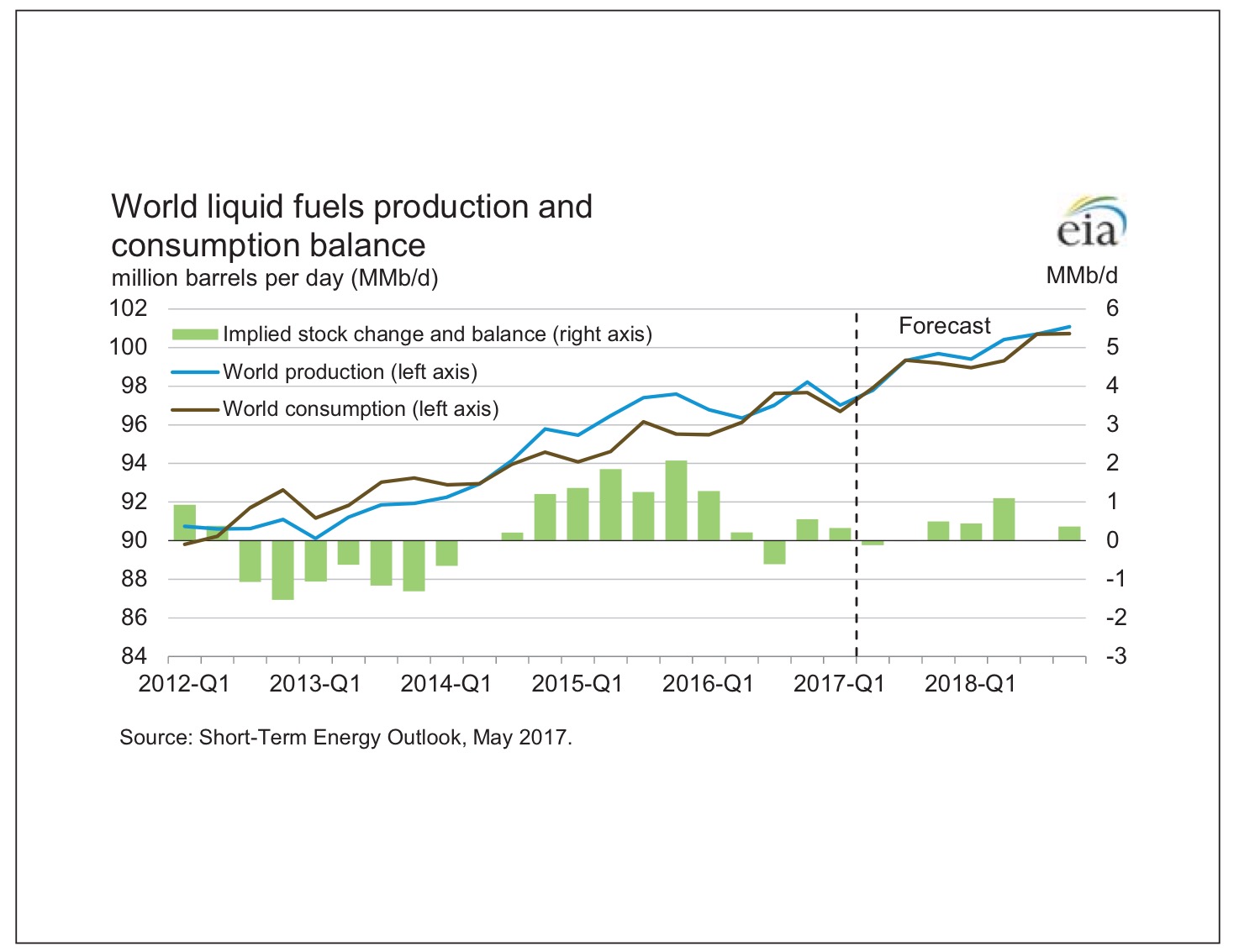

This chart shows supply/demand balance expectations:

Note that stocks aren’t expected to decline… Here is the EIA:

“Implied global petroleum and liquid fuels inventories are estimated to have increased by 0.4 million barrels per day (b/d) in 2016. EIA forecasts inventory builds to average 0.2 million b/d in 2017 and then increase to an average of 0.5 million b/d in 2018.”

The EIA raised supply estimates from last month:

“Growth in global liquid fuels supply is expected to limit upward price pressure over the next year. World liquid fuels supply is projected to grow by 1.4 million b/d in 2017 and by 1.9 million b/d in 2018. Compared with the April STEO forecast, those growth estimates are higher by about by 0.2 million b/d in 2017 and 0.1 million b/d in 2018. The upward revision to expected supply growth is based on higher expected crude oil production growth from the United States, Brazil, and Canada and more OPEC non-crude liquid production growth. Expected world liquid fuels consumption growth is largely unchanged from the previous STEO, with growth forecast at 1.6 million b/d in both 2017 and 2018.”

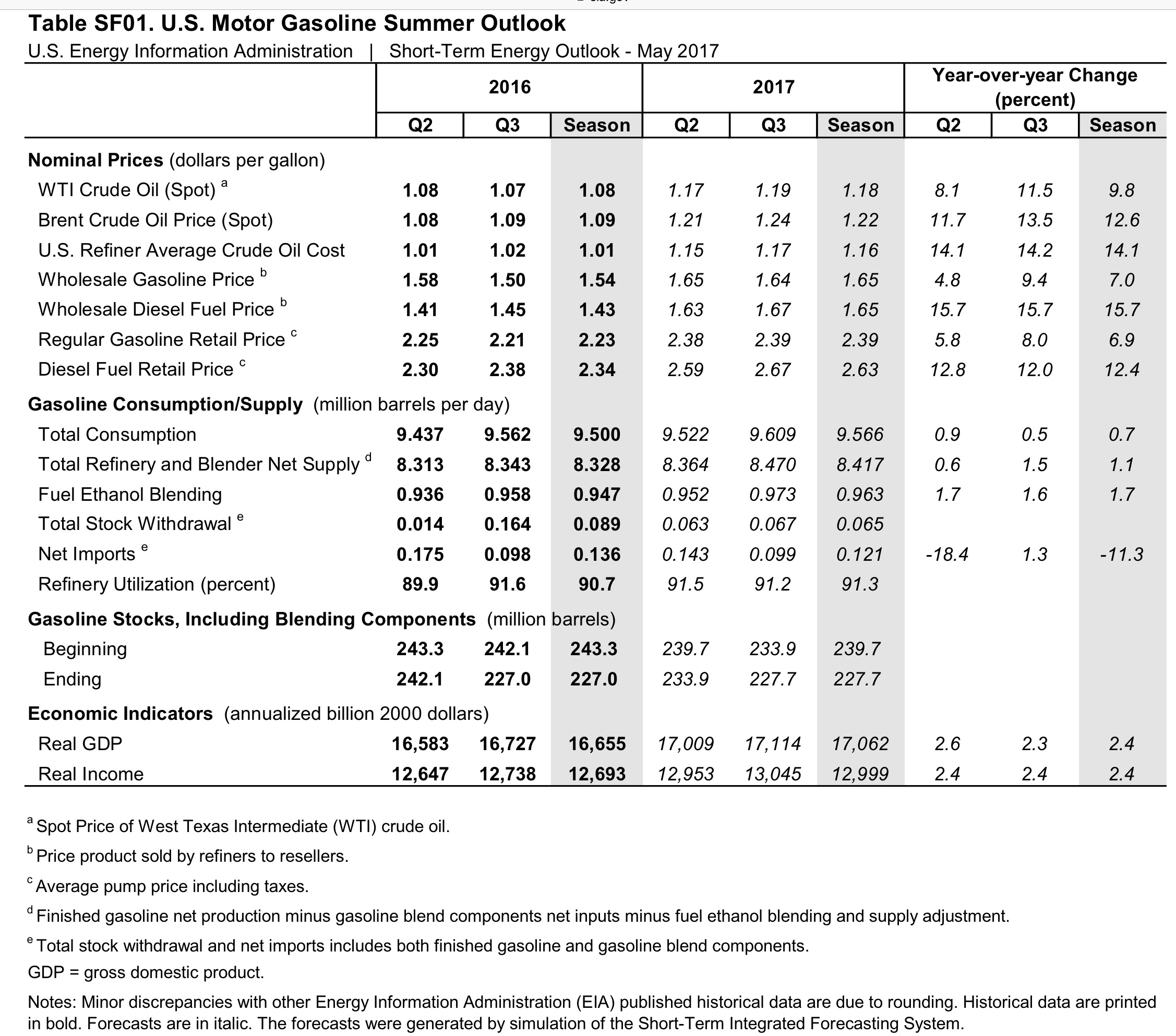

They include Q2 and Q3 estimates for gasoline demand, which seem very optimistic:

The recent Weekly Petroleum Status Report shows 4 week average gasoline demand running at 9.248, or 2.4% below last year! Note that the EIA estimates gasoline demand to be up 0.9% and 0.5% for Q2 and Q3 (year over year)… These numbers will be difficult to make even with revisions…

Leave a Reply