The options market is acting quite logically as an already tight market is hit with escalated isolation of a major oil exporter:

- Despite higher oil prices, implied volatility is rising sharply reaching 75.9% in April WTI and 63.4 in May.

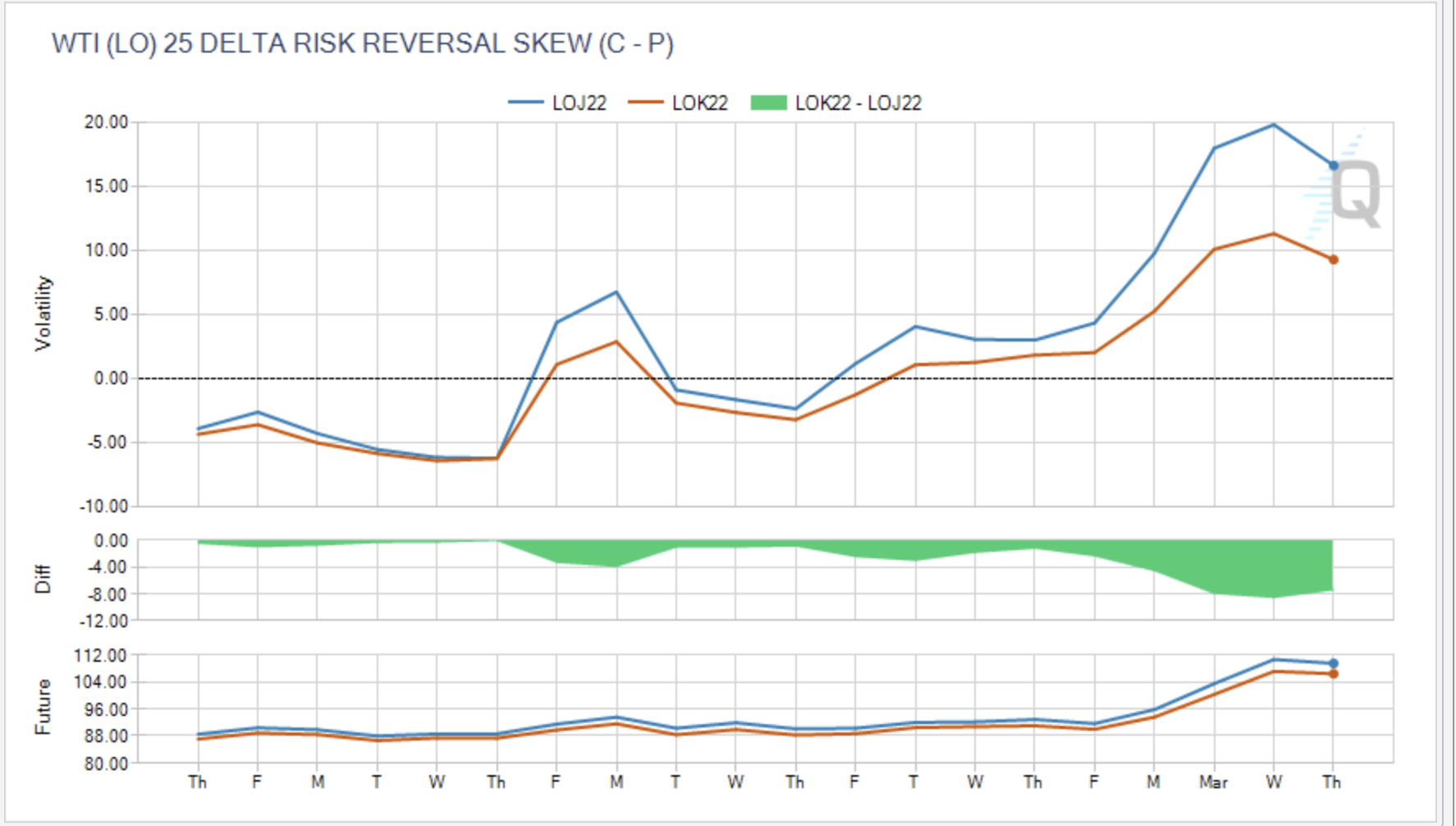

- The skew (out of the money call vol minus out of the money put vol) has move from a naturally bearish look (oil producers like Mexico hedge by buying puts) to a not normal bullish look (bullish skew periods do happen like the time when Iraqi barrels were off the market).

- Option volume is high. Yesterday was a typical day. Brent plus WTI calls trade 349,127 times, puts, 172,239. The odd part is that open interest in puts increased more than calls, +93,662 to +4,309. Some of this is likely due to profit taking, call rolling (many spreads are trading at close to net zero on open interest change) and producers hedging expansion plans with buy put strategies (why be exposed to a short futures positions during a war?).

Here is the skew chart from QuikStrike:

Leave a Reply