This is from the IEA’s summary, here…

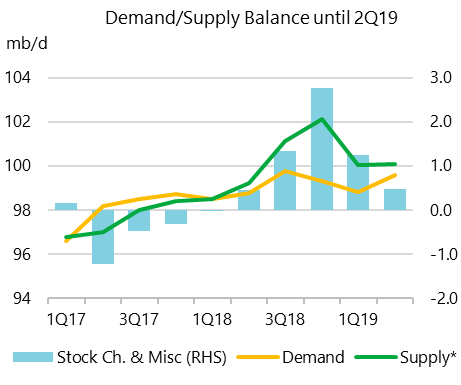

”The main message of this Report is that in 1H19 oil supply has exceeded demand by 0.9 mb/d. Our latest data show a global surplus in 2Q19 of 0.5 mb/d versus previous expectations of a 0.5 mb/d deficit. This surplus adds to the huge stock builds seen in the second half of 2018 when oil production surged just as demand growth started to falter. Clearly, market tightness is not an issue for the time being and any re-balancing seems to have moved further into the future.”

And this (my bold):

- Global demand growth is set to accelerate from an exceptionally weak 310 kb/d in 1Q19 and 800 kb/d in 2Q19 to reach 1.8 mb/d in the second half of the year as economic activity improves and petrochemical plants ramp up. For 2020, the pace of growth will average 1.4 mb/d compared to 1.2 mb/d this year.

- Our balances show the potential for oversupply next year, with a 2.1 mb/d expansion of non-OPEC supply, led by the US, versus 2 mb/d in 2019. That will lower the requirement for OPEC crude, with the call on OPEC plunging to 28 mb/d in 1Q20. OPEC has not produced at such a low level since 3Q03.

- Global refining throughput in 2Q19 dropped 0.7 mb/d y-o-y, the largest annual decline in 10 years. Our estimate for 2019 growth is revised down to 300 kb/d, but refined products stocks build nevertheless. East of Suez refiners are more exposed to products oversupply, while Atlantic Basin runs have fallen back to 2014 levels.

- OECD commercial stocks increased by 22.8 mb in May to 2 906 mb, and stood 6.7 mb above the five-year average. Preliminary data for June show inventories falling in the US and Japan whereas stocks increased in Europe.

- Concerns that global oil demand is slowing caused ICE Brent to decline by 10% in June, despite supportive geopolitical factors. Gasoline cracks picked up following a refinery fire on the US Atlantic Coast.

Leave a Reply