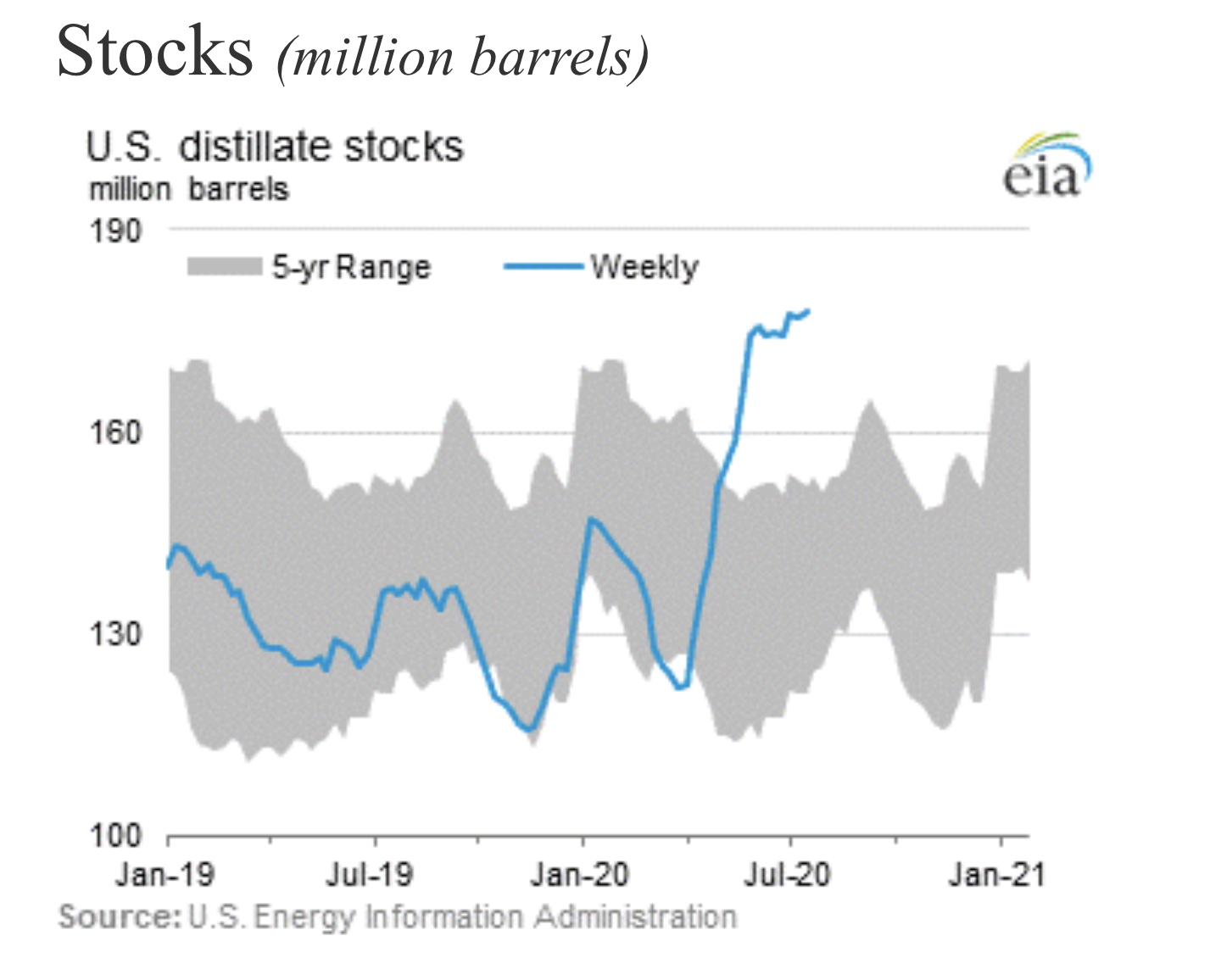

After looking at the EIA’s weekly stats, specifically the high level of distillate stocks, and price firm spread chart in Aug/Sep diesel, I asked Andy Lebow what was going on… Here is his response from earlier today:

”Cash is actually over the screen in NYHarbor. Inventories in Pad 1 have begun to decline as refiners continue to shave the distillate make. The HO/GO has come in to where exports from Europe don’t really work into Pad 1. The really big problem is in Pad 3 where there are post 1990 record distillate stocks. Latin America demand is horrendous crimping exports and the arb doesnt quite work to ship to Europe -although that is getting close if not workable. Cash down there is 450 under the screen. I would think it would even be worse but maybe the markets are telling us that export demand is picking up just a bit. US demand is not really picking up though as demand is 3.4 mbd for last 4 weeks-0.4 mbd behind last year. it’s slightly below the number I’m using for July and below 3.5 that the EIA had for July. We’ll see how the convergence goes on Aug expiration. Aug/Sep may go out even stronger than where it is now.”

Leave a Reply