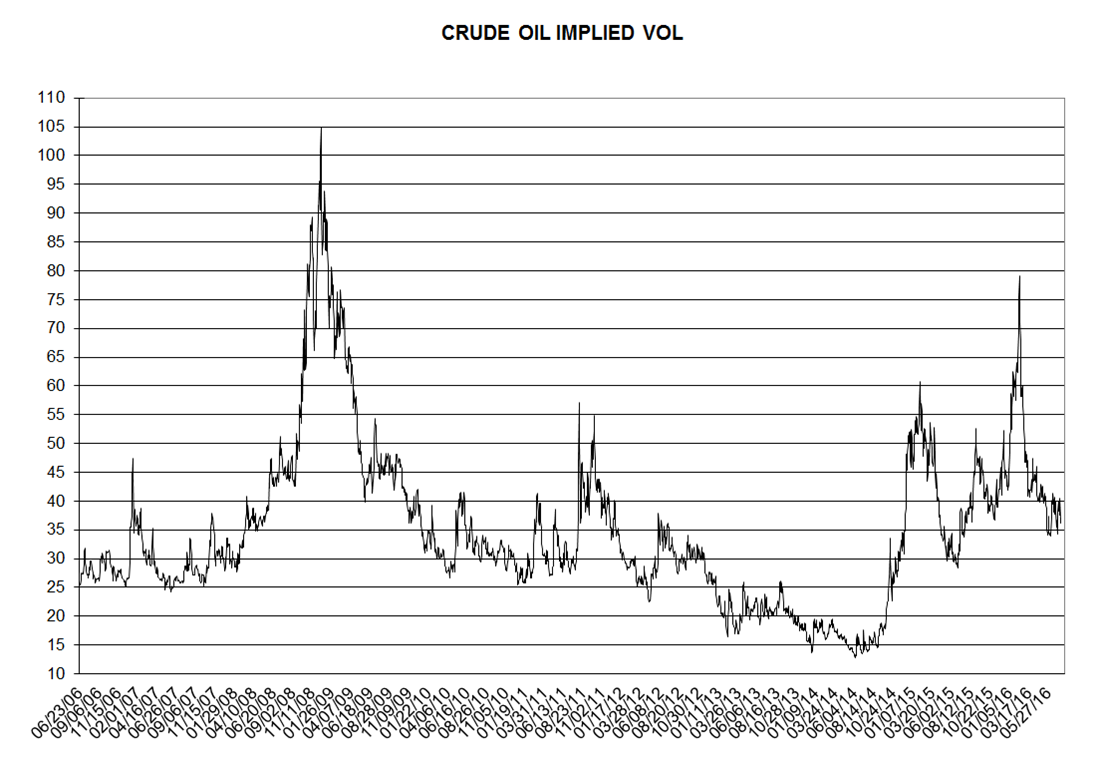

Implied volatility in crude oil has not been too interesting lately, with options trading in the mid to high 30’s for most of the last two months… Earlier this year, in February, we touched 79%… Options with the highest open interest are in December puts (30p, 47,663 contracts open; 45p, 39289; 40p, 37,567; 35p, 30,433) and September puts and calls (50c, 27,253; 40p, 30,601)… Activity in September 40p and 50c probably reflects a $40/$50 consensus trading range over the next month… In spread options, open interest is concentrated in -$1.00 puts for August and Sep; -$.75 puts for Oct, Nov and Dec16; and, -$.50 and -.35 puts for Jan through June 2017… $0 calls have most open interest going forward, led by over 20,700 for Dec16… Activity in spread options seem to trace out expectations of less contango going forward as active put strikes move higher out along the curve…

Here is the chart of implied vol for crude oil based on the at the money strike of the second nearby option, through July 18th:

Leave a Reply