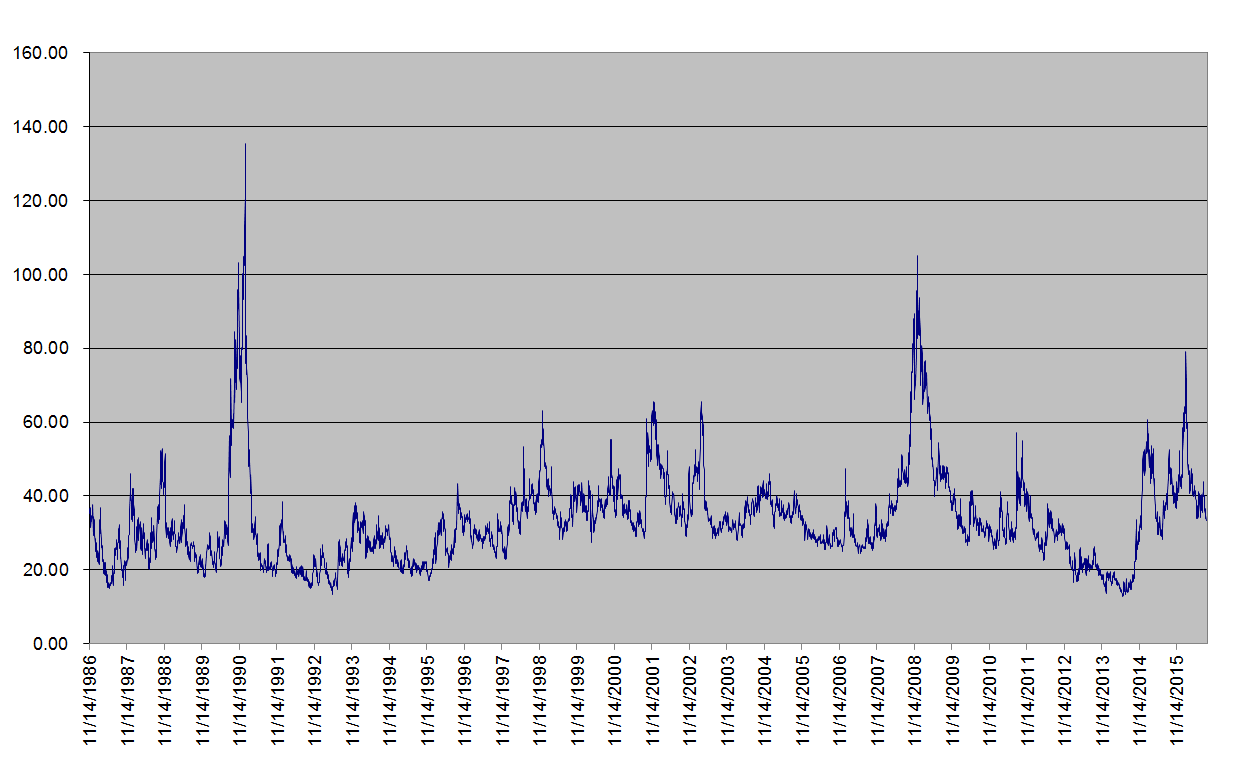

Implied volatility for WTI crude oil futures settled at 33.4% on Friday… The long term average implied vol since options began trading on the NYMEX is 33.2… Here is the long term chart:

November 14th, 1986 was the first day of trading… The first spike in vol was due to Gulf War I, just before bombs were dropped in Iraq; the second spike was in 2008 when prices dropped from around $145 to around $35; and, most recently, the implied vol spiked close to 80% in February this year…

Leave a Reply