Here is recent history from the EIA’s This Week in Petroleum:

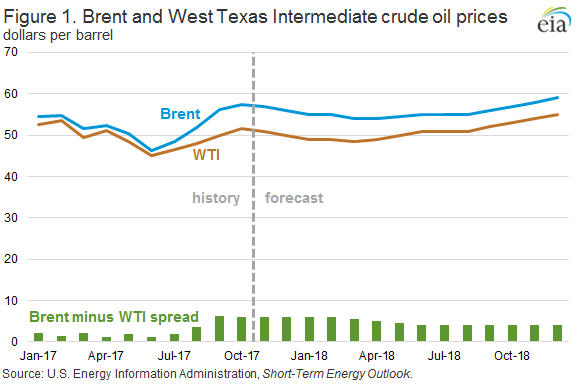

“The WTI price spread with Brent reflects the transportation costs associated with bringing crude oil from Cushing to the U.S. Gulf Coast and with exporting crude oil to Asia, the marginal market in which Brent and WTI crude oils compete.”…

“EIA estimates that, without pipeline constraints, moving crude oil from Cushing to the U.S. Gulf Coast typically costs $3.50/b, but it has gotten more expensive as transportation constraints have developed.”…

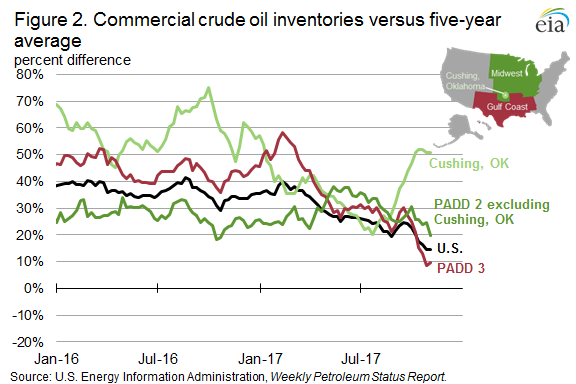

Here are stock levels showing a buildup of oil in Cushing, the delivery point for WTI futures:

And this:

”The remainder of the Brent-WTI spread is associated with transporting light sweet crude oil from the U.S. Gulf Coast to Asia. With the removal of restrictions on exporting domestically produced crude oil in December 2015, additional supplies of light sweet crude oil that cannot be economically processed at refineries or transported domestically can now be exported. Once exported, WTI competes with Brent directly in the global market. U.S. crude oil export data suggest that the marginal competitive market for WTI and Brent is in Asia. So far in 2017, China is the second-largest destination for U.S. crude oil exports at 173,000 barrels per day (b/d).”

More pipeline capacity will be needed to drain Cushing:

”Many other factors may influence the Brent-WTI spread, although those factors are likely to fluctuate and average out over the course of many months. EIA forecasts the Brent-WTI spread will remain at $6/b until the second quarter of 2018, when increased transportation capacity between inland crude oil production and the Gulf Coast is brought online.

These projects include the 0.4 million barrel per day (b/d) Midland-to-Sealy pipeline that will increase crude oil flows out of the Permian to the U.S. Gulf Coast when it becomes operational, currently planned for the second quarter of 2018. Other pipeline projects will increase Midwest refineries’ access to crude oils in the Permian region, potentially resulting in lower crude oil stocks at the Cushing pricing hub. Uncertainty associated with this element of the Brent-WTI spread forecast comes from potential changes in U.S. crude oil production growth rates and delays in pipeline completions. EIA expects that the additional transportation capacity between domestic crude oil production and the U.S. Gulf Coast will result in the Brent-WTI spread reverting to an underlying $4/b, based on estimated transportation costs and the costs of exporting to Asia.”

Here is the link:

https://www.eia.gov/petroleum/weekly/

Leave a Reply