The EIA’s Short Term Energy Outlook, here, has a nice chart showing some key oil spreads, with an explanation (my emphasis):

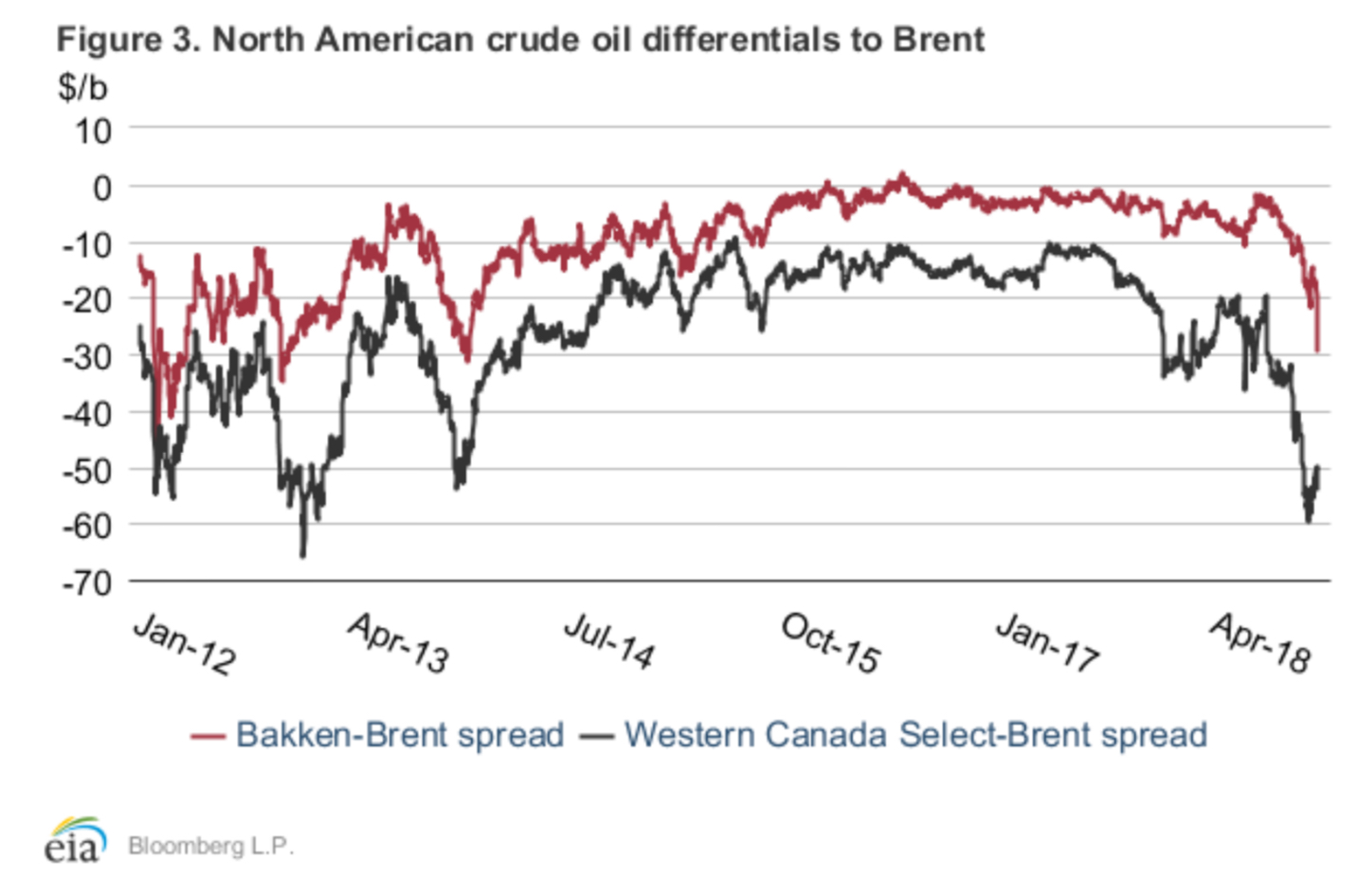

“Even though total U.S. refinery utilization was about average for this time of year, it was particularly low in the Midwest, Petroleum Administration for Defense District (PADD) 2. Four- week average refinery utilization for the week ending October 26 was 73%, which, if confirmed in EIA’s monthly data, would be the lowest utilization rate in the region for any month in EIA data back to 1985. Several large refineries planned month-long maintenance, which lowered the demand for and the prices of major crude oils that are typically processed in these refineries, including Western Canada Select (WCS) and Bakken. In October, the WCS–Brent spread traded at the lowest level since 2012, settling at -$53.88/b on November 1, and the Bakken–Brent spread hit its lowest level since 2013, settling at -$29.38/b on November 1 (Figure 3). Transportation constraints in Western Canada have resulted in more crude oil that must be delivered by rail, a more expensive option than pipelines, which further affects the crude oil discounts at a time of low refinery demand. In the Bakken region, available pipeline capacity could begin to face constraints as production in the region is estimated to approach 1.4 million b/d in November, an all–time high.

Leave a Reply