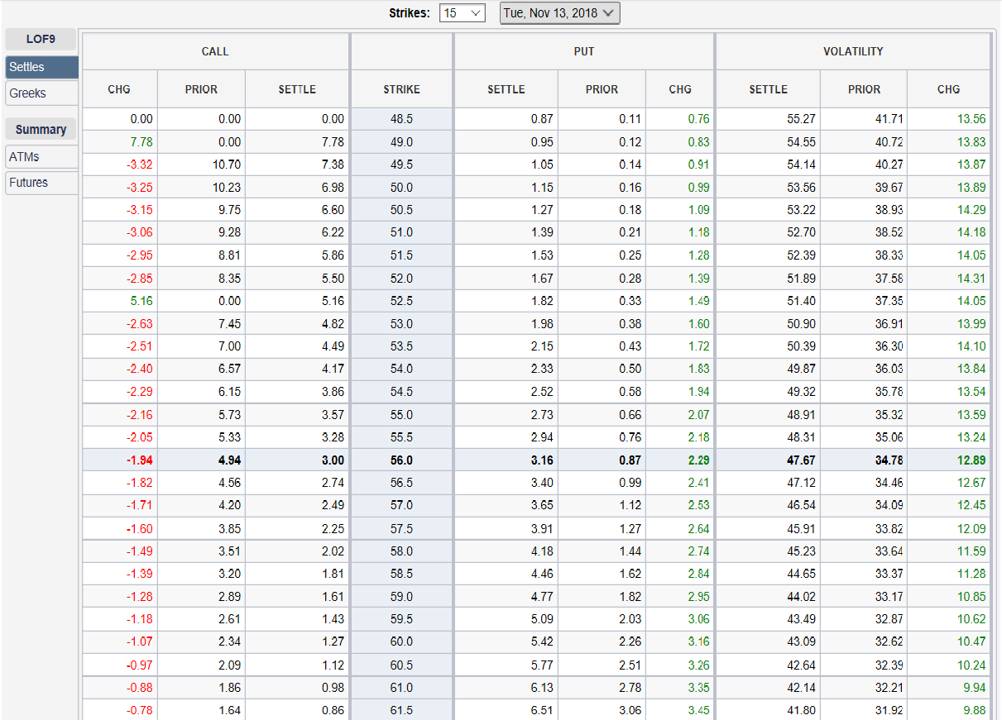

Natural gas and crude oil prices are moving in opposite directions… in a hurry… Implied vol for both have moved up sharply, with natural gas settling yesterday at 68.8 and crude oil at 47.7… Both of these were trading at around 25 in October… Using the CME’s Option Settlement Tool, here, we get a sense of how out of the money puts trade relative out of the money calls by looking at the skew… The skew is the difference between the implied volatilities of higher strikes vs. lower strikes… In crude oil, producers like Mexico, buy puts as price insurance… This causes out of the money puts to trade at higher vols than out of the money calls… Here is a snapshot of oil and natural gas implied vols across strikes… Note that oil is very skewed toward the puts and in natural gas the skew is toward the calls… For example the the $3.50 strike settled at 62.5 while the $4.80 call settled at 75.5… In crude, the $51 put settled at 52.7, the $61 call at 42.1… Theoretically, if the options model from which we calculate implied vol were a true depiction of reality, implied vol across strikes would be the same…

Leave a Reply